r/AskHistorians • u/Tatem1961 Interesting Inquirer • Mar 05 '25

Great Question! Credit cards were invented in 1950. Credit card readers were invented in 1979. During those 3 decades were cashiers writing down every customer's credit card number by hand?

1.4k

u/TywinDeVillena Early Modern Spain Mar 05 '25 edited Mar 05 '25

That would have been a tad complicated, but of course there was a solution: the credit card imprinter, or as we call it in Spain "bacaladera" (cod cutter).

Between the birth of credit cards and the advent of credit card readers, the method to be used was the imprinter and the slip of paper. With the use of multicopy paper, the operation of the imprinter became easy, comfortable, and reliable, issuing two identical copies, one for the customer and one for the shop or establishment in which the card payment was used.

Of course, this was not instantaneous as it has been for a long time with the use of information technology, and so there was a small window for fraud. Instead of going to the bank with every single payment slip, the shop owner, business manager, accountant, or person in charge of such tasks would take all the slips from the day at the start of the next day (banks don't open in Spain in the afternoons, normally) so that the bank would process them.

As a measure of preventing credit card fraud, the credit card companies issued every month a register of annulled credit cards, which the business owner would have at hand when someone wanted to pay by card. After making sure that the card was not on the register, the businessman would ask to see the customer's identity card to make sure that the card used actually belonged to him. If the purchase was too large (back in those days, if it was over 10,000 pesetas), the businessman would call the credit card company, whose number was on the registry, to ensure that the card had sufficient credit for the operation.

The card imprinters were used in Spain between the 1970s, when the bank cards became popular, and the mid 1990s and the advent of the magnetic stripe card readers. The imprinters or bacaladeras were not only used at shops, but also at medical offices to keep a registry of the patients coming and going in order to later invoice the insurance companies such as Adeslas, Sanitas, DKV, or any other. The imprinters and slips of multicopy paper are still available in a vanishing number of shops (in order to still take card payments in case of a sudden power outage) but they are still visible in medical offices.

Source: Hernández Bermejo, Fco. Javier (2018), "Análisis y gestión de los instrumentos de pago", IC Editorial, Antequera.

Edit: I should add, for clarity's sake, that the first credit card in Spain appeared in 1971, issued by Banco de Bilbao (nowadays BBVA) and BankAmericard (now Visa).

Edit 2: Here is an example of an imprinter and multicopy paper slips:

https://es.wallapop.com/item/antigua-bacaladera-visa-con-material-de-trabajo-1001135524

270

u/holomorphic_chipotle Late Precolonial West Africa Mar 05 '25

Your comment is making me feel extremely old. Twenty years ago it was not uncommon for Mexican supermarkets to keep a couple of those machines in reserve in case there was a sudden power outage (common after earthquakes). We called them "planchas" and my siblings and I managed to hurt ourselves playing with those things.

106

u/The_Chieftain_WG Armoured Fighting Vehicles Mar 06 '25

Wait until someone asks how airplane tickets were purchased in, say, the 1980s, with those thin triple-copy things... Then some of us will really feel old.

→ More replies (5)7

u/Timguin 29d ago

with those thin triple-copy things

What's that referring to?

→ More replies (1)11

u/The_Chieftain_WG Armoured Fighting Vehicles 29d ago

Something like this.

https://nationaltreasures.ie/submissions/GPDMIN→ More replies (30)18

u/steadyjello Mar 08 '25

I used one about 10 years ago when the credit card system at the restaurant I worked out went down.

→ More replies (1)553

u/ducks_over_IP Mar 05 '25

Fascinating! Is this why credit cards were embossed with raised letters and numbers for the longest time? It seems like only in the past decade or so (at most) that banks have started issuing credit and debit cards with flat-printed names and numbers, at least in the US.

→ More replies (16)595

u/TywinDeVillena Early Modern Spain Mar 05 '25

That is exactly the reason why the card info was embossed

→ More replies (3)187

u/EverythingIsOverrate Mar 05 '25

Great answer! Just as a little addition, according to my father, who was alive during this period, credit card imprinters were colloquially called "knuckle-busters" in English, which a quick Google confirms.

→ More replies (20)86

u/TywinDeVillena Early Modern Spain Mar 05 '25 edited Mar 05 '25

Good to know! I was sure there must have been a colloquial English term but I didn't know it. In Spain the term "bacaladera" comes from the type of motion used for imprinting the card information onto the multicopy paper, which is similar to what you would do to take the scales off a piece of cod.

→ More replies (2)47

u/AchillesNtortus Mar 05 '25

To add to your point:

If the purchase was too large (back in those days, if it was over 10,000 pesetas), the businessman would call the credit card company, whose number was on the registry, to ensure that the card had sufficient credit for the operation.

There was also another anti fraud control. As a merchant you were given floor limits as well which varied from business to business and from week to week. For example you would have to call for authorisation if the charge was over £50, or between £10 and £22. This was to catch the thieves who would go from business to business and who were aware of the maximum purchase amounts.

There was both a carrot and stick to this. Failure to seek authorisation would mean the merchant would be stuck with the costs of the fraud. There were also rewards for spotting and reporting fraud.

This strategy is still used with contactless cards. You may be asked to enter a pin code sometimes which is well below the contactless limit. I suspect this method is more variable than the old weekly notices

→ More replies (2)

265

u/xiaorobear Mar 05 '25 edited Mar 05 '25

I see the claim that credit card readers and magnetic stripes were invented in 1979 on the internet, but I don't believe it is accurate. IBM created a standard for magnetic stripes in 1969, and they were put into some limited use starting in 1970, and gained wider use especially in banking quickly despite different companies taking a few years to argue over standards. Here is a photo of someone using an IBM Transaction Validation Terminal to pay via credit card in 1971, from IBM's website. By 1973, 85% of all credit cards used magnetic stripe technology, per The Credit Card Industry: A History by Lewis Mandell (1990), even if not all retailers would have a machine to read it. The following info is also from that book:

{kind=link}

The technology to copy customer info down all at once existed prior to the universal credit card- starting in the 1920s some retailers used "charga plates," embossed metal tags with a customer's name and address on them, put into an imprinter device. Then you pressed down a paper form and ink, or a carbon paper form, over them, and got a copy of all the info without having to write it out by hand. Sometimes the charga plates were just kept by the business and used for repeat clients, rather than something the client carried around on their person.

{kind=link}

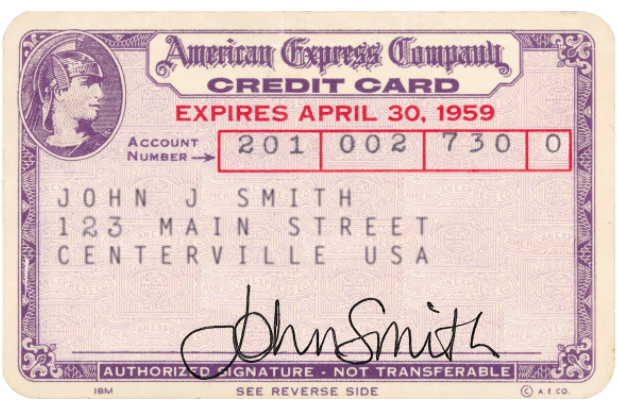

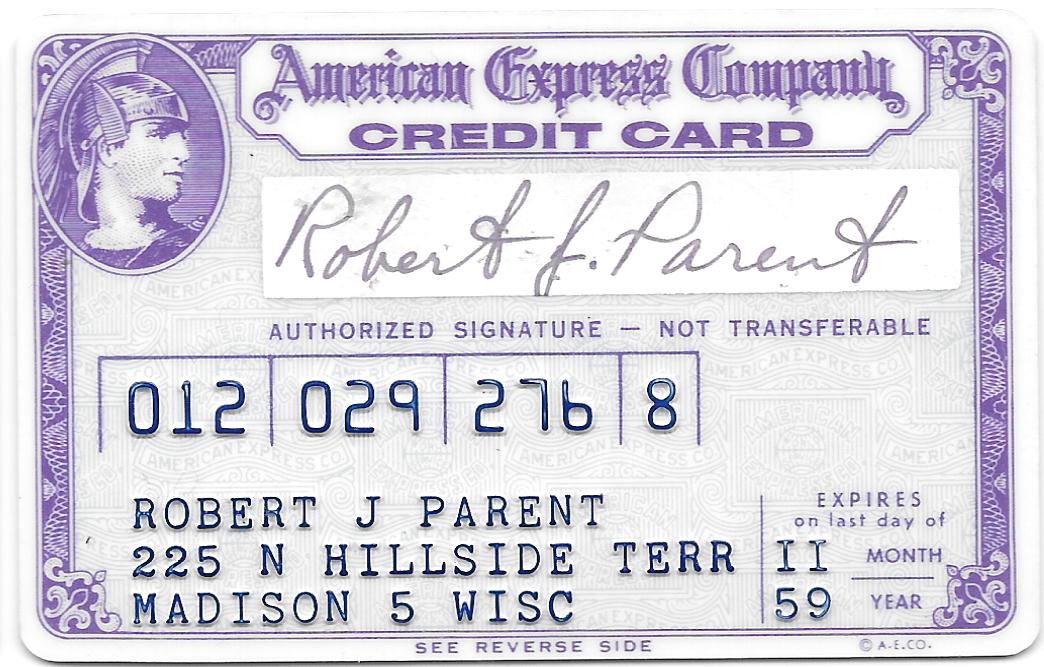

Credit cards didn't start using this method until 1959. In 1958 for example, here is the first Amex Card, made of cardstock, with the info stamped on in ink- this would have to be copied by hand. In 1959 Amex and Bank Americard started issuing cards made of plastic, with embossed letters and numbers pressed into them. So then credit card imprinters, following the same methods used to copy earlier embossed info, were able to make carbon copies of all the info on the card, giving the business and the customer a receipt. This would remain the backup system for if the magnetic stripe (or OCR) card reader systems went down for decades.

{kind=link}

{kind=link}

→ More replies (1)80

u/TywinDeVillena Early Modern Spain Mar 05 '25 edited Mar 05 '25

Very interesting to read how things were in America. As you may see from my answer, credit cards arrived quite noticeably late to Spain compared to the US

→ More replies (2)72

u/xiaorobear Mar 05 '25

Interesting indeed, yours is a great comment! In 1970 apparently only 16% of US households had a credit or bank card. So even though things were a bit ahead, the majority of people in the country were not using them. I think it wasn't until the mid 80s or early 90s that the majority of households in the US had a credit card.

→ More replies (2)50

u/TywinDeVillena Early Modern Spain Mar 05 '25

Just for fun, I'll give you an odd bit of info: the first church in Spain to have a card reader for donations was the church of San Claudio, in León. They installed it in 1995, and the cathdral set up one the next year.

That year was when magnetic stripe card readers became the norm and imprinters started to be on the way out.

60

u/police-ical Mar 05 '25

The basic concept of *individual* credit at retailers is quite old. This is one aspect of life prior to credit cards that has been virtually forgotten, yet shows up plenty in older media and sources. If you lived in a small town in the U.S. and were a regular at the local grocer, you likely didn't pay cash or check every time. They added your balance "to your tab," noting it on a ledger, and you'd pay the full tab periodically. This allowed for flexibility around pay day, decreased need to deal with cash and change, and functioned well enough in a setting where social norms against nonpayment could be implicitly enforced, i.e. a town where people knew both you and the grocer. Merchants did have to deal with a certain amount of nonpayment and tabs getting too high, particularly in economic downturns, but my impression is this also functioned as a limited form of charity. People short of cash could still get food for the time being and some tabs might chronically run a little over-extended.

To this end, the earliest "credit cards" were a natural extension of store credit, where a specific retailer like a department store would give you a card (or another object) with your account number on it, making it a bit easier to keep track of purchases, while also acting as a little nudge towards repeat business. This really wasn't that much of a technical advance, just a bit of streamlined bookkeeping. For that matter, even once we switched to magnetic strips, the card itself was really just a piece of identification with a few pieces of information. The biggest innovations were in creating an effective network that could allow one card to be accepted most places a person would buy something, AND do this quickly and efficiently so that a card would be no harder than cash or check.

This wasn't easy. Barriers to entry were considerable. One was a natural problem: Merchants didn't want the hassle and expense of accepting one more method of payment unless it was so popular that it more than paid for itself, and customers didn't want to bother to adopt a new method of payment unless it worked most places. Moreover, you now had to figure out how to verify a potentially enormous number of transactions and prevent fraud, while trying to keep things moving.

So, this is the practical part. To OP's question, the raised numbers on the card allowed them to be easily copied onto carbon paper by an imprinter, basically just a simple machine that could slide/press it firmly. The carbon paper would also have room for an authorization code which had to be obtained by calling the credit card issuer directly; a person there would confirm a valid account that was below its credit limit. The whole process would yield one receipt apiece for merchant and customer, as well as a slip to be sent to the bank so that the merchant would actually get their money in a few days. Merchants also routinely compared your signature to the card signature and get additional identifying info like a driver's license. The other fraud protection mechanism was checking your card number against a regularly-updated and thick book of known fraudulent/invalid numbers.

So, there was no need to write numbers, but it could mean one phone call per transaction AND an authorization code to write down AND manually confirming multiple safeguards. The simple workaround was that small sums were often simply assumed not to be worth the hassle of verification and could be run on good faith alone. However, sums above a certain threshold (I've seen $20-$50 in various sources and would assume this changed rapidly over the course of 1970s inflation) required verification. You can see why cards didn't really supplant other forms of payment until the process was automated.

Now, what happened after the transaction itself? That slip went to the merchant's "acquiring bank" (i.e. the one that processed transactions on merchants' behalf) which routed it to the relevant credit card network, which sorted incoming slips by "issuing bank" (i.e. the consumer bank that put out the credit card) and sent a bundle of slips to each bank, which received them and debited each consumer's account. Then as now, the consumer paid their bill periodically.

By this point you may be noting how much work and paper this all seems like. That's correct. When you see a phrase like "automated clearinghouse," this is the kind of thing computers came to replace: Complex and labor-intensive places where actual people sorted a whirlwind of paper information by hand.

Mercifully for consumers and the people processing credit cards alike, this is a time when cash remained king for ordinary purchases. A wallet full of $20 bills had decent purchasing power. Common options like financing/installments/layaway were common and meant breaking large purchases into small-ish monthly amounts--many early televisions were bought at $10-$15 a month. Checks were an option but check fraud was in its heyday, so checks from a out-of-town bank might be regarded with particular suspicion or not accepted.

6

u/Tatem1961 Interesting Inquirer Mar 07 '25

Thanks! It's interesting to see the full process of how it worked!

This wasn't easy. Barriers to entry were considerable. One was a natural problem: Merchants didn't want the hassle and expense of accepting one more method of payment unless it was so popular that it more than paid for itself, and customers didn't want to bother to adopt a new method of payment unless it worked most places.

Do we know which side of this chicken and egg problem got solved? How did credit cards gain wide adoption amongst both businesses and customers?

→ More replies (2)→ More replies (2)4

u/ilfulo Mar 06 '25

Sometimes redditors provide a perfect answer. It's rare, but it happens. Thanks!

99

16

7

7

5

u/AutoModerator Mar 05 '25

Welcome to /r/AskHistorians. Please Read Our Rules before you comment in this community. Understand that rule breaking comments get removed.

Please consider Clicking Here for RemindMeBot as it takes time for an answer to be written. Additionally, for weekly content summaries, Click Here to Subscribe to our Weekly Roundup.

We thank you for your interest in this question, and your patience in waiting for an in-depth and comprehensive answer to show up. In addition to the Weekly Roundup and RemindMeBot, consider using our Browser Extension. In the meantime our Bluesky, and Sunday Digest feature excellent content that has already been written!

I am a bot, and this action was performed automatically. Please contact the moderators of this subreddit if you have any questions or concerns.

1

•

u/jschooltiger Moderator | Shipbuilding and Logistics | British Navy 1770-1830 Mar 05 '25

Hello everyone,

If you are a first time visitor, welcome! This thread is trending high right now and getting a lot of attention, but it is important to remember those upvotes represent interest in the question itself, and it can often take time for a good answer to be written. The mission of /r/AskHistorians is to provide users with in-depth and comprehensive responses, and our rules are intended to facilitate that purpose.

In particular, in this thread, we don't want a sentence or two that says "stores had machines that went ka-chunk and created a copy of the card numbers." Presumably OP can google that. What we're looking for is the process by which that process was created, how information was verified at banks, why the store and the purchaser and a bank got a copy, and how those were reconciled. If you can provide that, please feel free to post; if not, please do not!

We remove comments which don't follow them for reasons including unfounded speculation, shallowness, and of course, inaccuracy. Making comments asking about the removed comments simply compounds this issue. So please, before you try your hand at posting, check out the rules, as we don't want to have to warn you further.

Of course, we know that it can be frustrating to come in here from your frontpage or /r/all and see only [removed], but we thank you for your patience. If you want to be reminded to come check back later, or simply find other great content to read while you wait, this thread provides a guide to a number of ways to do so, including the RemindMeBot- Click Here to Subscribe - or our Bluesky.

Finally, while we always appreciate feedback, it is unfair to the OP to further derail this thread with META conversation, so if anyone has further questions or concerns, I would ask that they be directed to modmail. Thank you!