President Donald Trump’s so-called Liberation Day is coming on April 2, with the launch of his new reciprocal tariffs. Investors are hoping for freedom from the cloud of uncertainty that has been hanging over the economy.

As Federal Reserve Bank of Richmond President Tom Barkin put it last week in explaining monetary policymakers’ cautious new outlook, “How does one drive in fog? Carefully and slowly.”

But the fog may lift only to roll right back in. The details of those tariffs won’t be the last policy hit to the market from the new administration. Politics is creeping into the market through just about every asset class—and more than usual, some experts say. The markets for U.S. Treasuries and gold, and to some degree in stocks, are dependent on the fragile mood in the country and the fight over political institutions.

The U.S. is “basically looking more and more like an emerging market,” political scientist Mark Rosenberg says.

“You have higher policy uncertainty, you have greater questions about rule of law, you have concerns about the ability of the state to tackle its fiscal problems, a dysfunctional political environment,” Rosenberg says. “All the stuff that you would get if you were talking about South Africa or Brazil.”

Rosenberg’s firm, GeoQuant, builds models of political risk. It quantifies legal, social, and other similar sources of data for countries around the world, including the U.S. His clients use those indicators as early-warning signs of risk in countries of interest and as aids in portfolio allocation. Fitch acquired the company in 2022.

The difference between developed and emerging markets for Rosenberg is in how much politics matters to market outcomes. “In an emerging market, elections matter a whole lot more,” Rosenberg says, “because the underlying social instability and institutional uncertainty mean that a political contest like an election can produce a very large policy swing and/or a changing of the rules of the game for the political economy, which you just would never anticipate in a developed market.”

Policy just about always changes in the U.S. after an election, and uncertainty is natural. April 2 is tariff day because April 1 is the deadline for a set of trade reports and investigations that will determine tariffs’ legal and policy basis. (Also, the president wanted to avoid April Fools’ Day.) Normal enough.

Then, apparently, everything gets filtered through Trump’s personal feelings about world leaders. Canada’s Justin Trudeau gets called “governor” in a “joke” about the 51st state, while Mark Carney, who now leads the same party and has the same job, is “prime minister.” Meanwhile, U.S. companies need to jump through new regulatory hoops to get their exports certified under the USMCA trade deal so they can avoid 25% tariffs.

There are always periods of extreme politics under any president. But you don’t usually have that alongside the kind of battle that is going on over Elon Musk. And that one goes straight to the deficit. The Tesla CEO is also running DOGE, an initiative to slash government spending.

The “Tesla Takedown” drew protesters around the country on Saturday, animated by opposition to cuts to the federal government driven by Musk and DOGE. That protest movement has accelerated despite warnings from officials such as U.S. Attorney General Pam Bondi, who on March 18 said “violent attacks on Tesla property” are” “nothing short of domestic terrorism.” (Nonviolent protest is a constitutional right.)

Tesla’s market capitalization has fallen by $500 billion since the Jan. 20 Inauguration.

But Musk is also the administration’s point man for cost-cutting. He and DOGE are the only hope for deficits to fall since Congress’s latest plans to extend expiring tax cuts would raise the deficit by $2.8 trillion. His fate as DOGE head is tied to the rate of the nation’s interest payments now.

Yields on government debt typically move up and down with investors’ expectations of growth and inflation. Social and political issues play a role in driving rates, too. They are helping to drive rates higher than might otherwise be expected.

Yields on 10-year Treasury notes have declined from 4.8% in January to near 4.2% largely because expectations for growth are falling. But they are still higher than they have been since the 2008 financial crisis.

“If you want to explain where Treasury yields are now, and you take the core macroeconomic factors at their face, there’s still a pretty big gap between what those factors would predict and where we are now,” Rosenberg says.

Bond veterans have noticed an unusual pattern in yields. “If you look at moves in the 10-year Treasury, now we have more 10-basis-point moves than we’ve seen since right around the global financial crisis,” says Gregory Peters, co-chief Investment officer at PGIM Fixed Income. A basis point is one-hundredth of a percent.

The dramatic rate shifts suggest that investors and central bankers are dealing with “policy-driven schizophrenia,” he says.

Gold keeps rising in price, a trend Rosenberg says is likely to continue along as the policy mess continues. The metal hit a record high Friday.

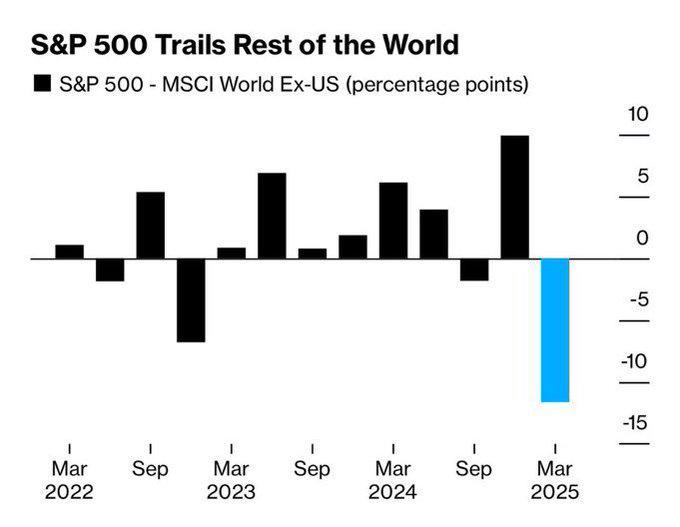

The hit from tariffs over recent weeks suggests that equity investors are nursing a political hangover, too. The S&P 500 is down 9% from its record closing level.

Investors aren’t all rushing to change their trading strategies. “From a bond guy’s perspective, an emerging market is one where when the economy slows, the government’s rates go up, and vice versa. I think we’re still a developed market,” says Campe Goodman, a fixed-income portfolio manager at Wellington.

The worry about this talk of emerging-market status is that it is hard to rebuild trust once it disappears. Global investors are still eager to hold oceans of U.S. government debt for relatively low rates. Why make them think twice about it?

Source: Trump’s Tariffs Are Turning the U.S. Into an Emerging Market - Barron's

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}